Why this comparison matters on the Gold Coast

If you are weighing up a bank branch against a gold coast mortgage broker, you are not alone. Local buyers in Surfers Paradise, Robina, Coomera, Burleigh Heads, and Nerang face tight timelines, complex policies, and fast moving prices. Using a broker changes your home loan search in practical ways. A broker compares options across many lenders. A bank can only offer its own products. Brokers in Australia must also act in your best interests when recommending a loan, which gives you an extra layer of protection as you decide. That legal duty sits alongside the service most people want in a hot market: clear guidance, help with paperwork, and faster progress from offer to approval.

On price, the difference rarely comes down to a headline rate alone. Lenders use discretionary discounts and policy exceptions that a local broker can often access by presenting your file well. That can be the difference between a quick yes and a drawn out maybe. The national competition regulator has also reported that pricing can be opaque, which is another reason buyers shop around or use a broker to negotiate.

Key Takeaway

A bank sells its own loans. A broker compares many and must act in your best interests, which can improve pricing transparency and approval odds for Gold Coast buyers.

Broker vs bank: what changes for a Gold Coast buyer

Choice and strategy

A broker can map your borrowing strategy across multiple lenders. That matters if you are a first home buyer using grants, an investor planning the next purchase, or a family upgrading in a specific school catchment. A bank adviser works within one lending policy. A broker can pivot if a lender’s appetite for your property type or postcode is limited. This flexibility is useful in high rise pockets of Surfers Paradise or compact townhouses in Coomera where some lenders have different settings for maximum exposure or minimum floor area.

Cost to use a broker

Most Australian borrowers do not pay a direct fee for residential broking. The lender pays a commission when your loan settles. You should still ask your broker to explain how they are paid and whether any fees apply in your case. Government consumer guidance also reminds borrowers that brokers must explain rates, features, and fees in plain language so you can compare value.

Pricing and negotiations

Banks set public rates but may apply case by case discounts. The ACCC has highlighted how these discretionary discounts affect transparency and switching. A broker can often ask the lender’s pricing team for sharper terms at the right moment, such as just before settlement or at a planned refinance review.

Policy fit and exceptions

Approval hinges on policy. For example, overtime income, probationary employment, casual hours, or self employed income each have different shading rules by lender. A broker can route you to a policy that fits rather than trying to bend one lender’s rules.

Service and speed

Brokers manage the flow of documents, valuation booking, and lender follow ups. That saves time, which matters if your contract has a short finance clause. Faster does not mean sloppy. A complete application with the right supporting documents almost always moves quicker than a light file with gaps.

When a bank may be the better pick

There are scenarios where going direct can make sense. If you already bank with a lender that offers a unique package for your exact situation, or if you need a product that only that bank offers, staying in house may be fine. But compare. Ask your broker to show you how that offer stacks up against the market.

Key Takeaway

Use a broker when you want wider lender choice, help with policy fit, and someone to manage the moving parts. Go direct if a specific bank product uniquely suits you and still compares well on price.

The local lending backdrop: what the rate cycle means for you

Interest rates shape borrowing power and repayments. The Reserve Bank of Australia sets the cash rate, and lenders adjust mortgage rates in response. Check the current rate path before you fix or float, or when planning a refinance. On the Gold Coast, this is especially relevant for investors and upgraders who want to stress test repayments against a realistic rate range.

If rates soften, consider keeping repayments at the higher level you are used to. That accelerates principal reduction and can shorten your loan term. If rates rise again, plan buffers into your budget. Your broker can run scenarios for both cases across multiple lenders so you can pick a structure that feels safe.

External reading: See the Reserve Bank’s cash rate history to understand the direction of travel. RBA cash rate target.

Key Takeaway

Rates move. Structure your loan so you can handle a higher rate, and use any drop to pay down faster. A broker can model both paths with several lenders.

Approval speed on the Coast: how to get to “yes” sooner

Gold Coast contracts often include short finance timeframes. Here is how to keep momentum.

- Sort ID and income early. Two photo IDs, two most recent payslips, last year’s tax documents, and any bonus or allowance proof. Self employed borrowers should add two years of financials where possible.

- Clean bank statements. Explain any large transfers. Reduce afterpay and credit limits that you do not use.

- Show genuine savings. A three month pattern strengthens first home applications. Some lenders accept rent as genuine savings with clear evidence.

- Pick the right lender for your timeline. Your broker will know which lenders are assessing files faster this month and which need extra time for valuations or credit sign off.

- Order valuation at the right time. For a tight contract, many brokers front load valuations to cut days off the clock.

- Keep your file stable. Avoid new debts, job changes, or moving money between accounts without telling your broker.

Data table: your pre-approval and approval checklist

| Step | What you need | Who does it | Typical time | Tips for the Gold Coast |

|---|---|---|---|---|

| Identity and income | ID, payslips, tax docs | You | 1 to 3 days | Save PDFs in one folder to share once |

| Living expenses | 3 month transaction history | You + broker | 1 day | Flag any unusual items upfront |

| Lender selection | Shortlist 2 to 3 lenders | Broker | 1 to 2 days | Match policy to your property type |

| Submission | Signed application, consents | Broker | Same day once complete | Double check all declarations |

| Valuation | Access and report | Lender panel | 1 to 5 days | Tenanted or off the plan may take longer |

A gold coast mortgage broker will sit on top of this process and push things forward. The extra lift from someone who knows each lender’s queue can shave days off a contract.

Key Takeaway

Speed comes from complete documents, policy fit, and smart sequencing. Ask your broker to front load anything that saves days on your finance date.

First home buyers: grants, concessions, and what to expect

Buying your first home is a big moment. Queensland offers targeted help for eligible buyers. The First Home Owner Grant can reduce your funding gap if you are buying or building a new home. You should always check the latest rules, limits, and timeframes on the Queensland First Home Owner Grant site before relying on any figure.

Transfer duty is another lever in your budget. Queensland provides concessions for eligible first home buyers and other home buyers. Concessions depend on price thresholds and intended occupancy. Read the current thresholds and rules for Queensland transfer duty concessions.

A broker can fold both incentives into your plan. They will also explain Lenders Mortgage Insurance if you have a deposit under 20 percent, and help you build a path to avoid or reduce it where possible. That might include a parental guarantee, a staged savings plan, or using eligible concessions to bridge the gap.

Key Takeaway

Check the latest grant and stamp duty settings on official Queensland sites. Then ask your broker to model them into your contract plan so your cash at settlement is clear.

Suburbs and “lowest mortgage rates” on the Coast

Buyers often ask which Gold Coast suburbs have the lowest mortgage rates. Lenders do not price loans by suburb. Your rate depends on the product, loan to value ratio, your credit profile, and any package discounts you qualify for. A broker may still steer you toward or away from certain properties based on lender policy. High rise apartments in parts of Surfers Paradise can have minimum size rules. Some lenders have maximum exposure limits in a single building. New builds in growth areas like Coomera sometimes need extra valuation care. None of this changes your rate directly. It can affect whether the lender will say yes and how fast.

How to use this insight when choosing suburbs

- Shortlist based on lifestyle and budget first.

- Share addresses with your broker before you sign.

- Ask whether that building or townhouse style has any lender quirks.

- If two properties are equal for you, prefer the one with a smoother valuation path.

A gold coast mortgage broker can flag these issues early so you avoid nasty surprises after you go under contract.

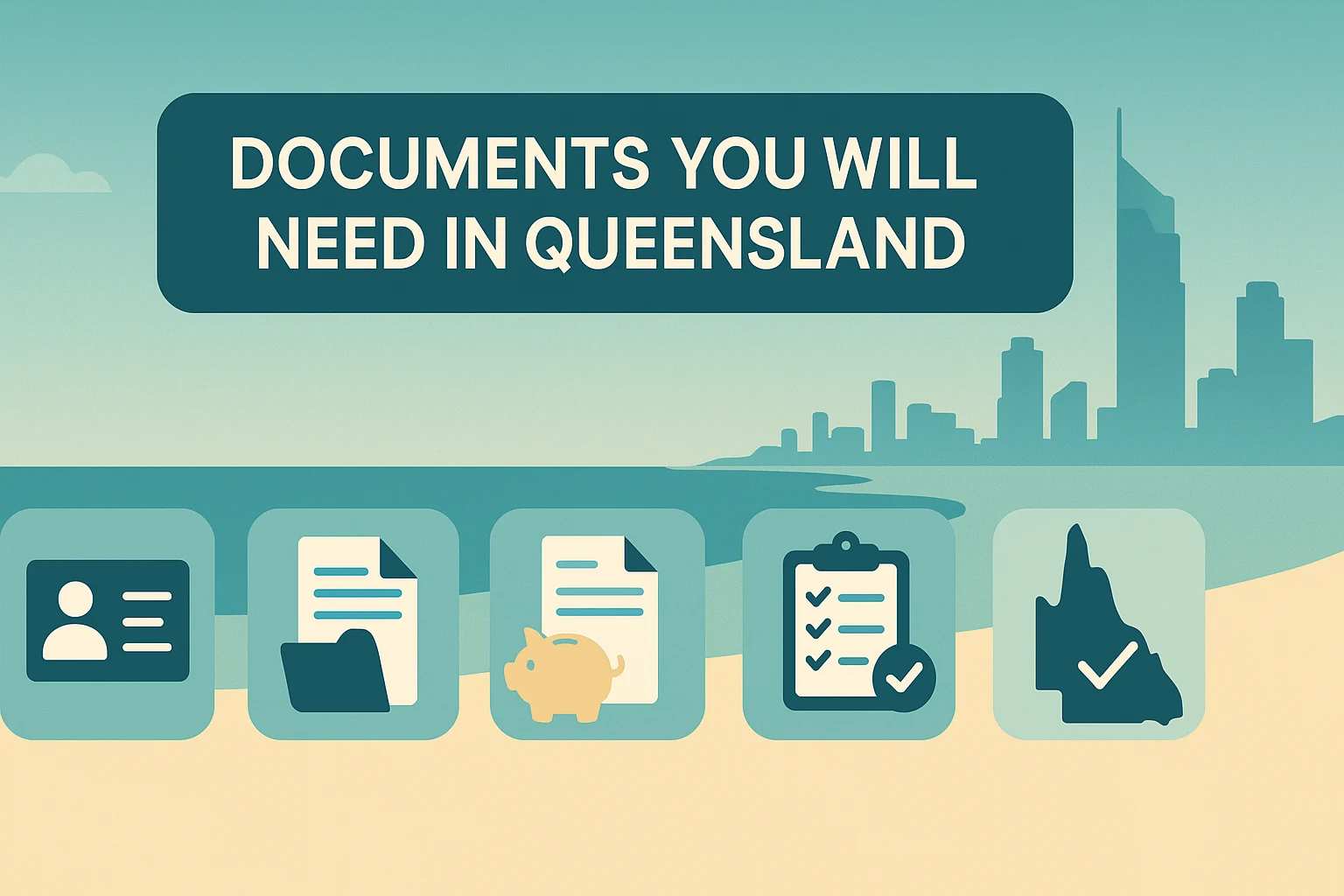

Documents you will need in Queensland

Every lender is a little different. Most will ask for the following.

- Photo ID for all applicants.

- Income proof. Employees provide payslips and tax info. Self employed provide tax returns, notices of assessment, and business financials.

- Living expense summary and 3 months of bank statements.

- Evidence of deposit. This can be savings statements, rental ledgers, or a gift letter if relevant.

- Contract of sale when you secure a property.

- Building and pest and insurance details before settlement.

Government sites and consumer guides encourage you to ask your broker to explain how each loan works and what it costs. Use that advice to keep your file complete and clean.

Broker vs bank for specific scenarios

First home buyers

A broker can line up grants and concessions, pick a lender that accepts your type of savings history, and plan around short finance clauses that are common on the Coast. They can also guide you on how to get your offer accepted. Use the official grant and duty links above to confirm current settings, then get a lender plan that fits.

Bad credit or thin files

If you have a late payment or a short employment history, a broker can present context and select a lender that reads your situation fairly. This is not about hiding problems. It is about packaging the story with documentation so a credit assessor can say yes with confidence.

Refinancing in Robina or similar hubs

If you want to release equity for renovation or lower your repayments, a broker will compare rates and cash back offers across lenders, then manage discharge timing so your switch is seamless. They can also calendar regular pricing reviews so you do not drift above market over time. The ACCC’s switchability findings make this discipline worthwhile.

Investors in growth pockets like Coomera

Policy choices matter for investors. Interest only periods, offset accounts, and fixed or variable splits change cash flow. Rental evidence and acceptable lease types differ by lender. A broker who writes lots of investor loans can help you structure for the next purchase.

Upgraders in family suburbs

Families moving to bigger homes often juggle a sale, a purchase, and a bridging loan. A broker can set up bridging so you can buy before you sell, or advise when a conditional contract is safer.

Gold Coast home loan FAQs

Who is the best mortgage broker in Gold Coast for first home buyers? There is no official single best. Look for a gold coast mortgage broker who writes a lot of first home buyer loans, can explain grants and concessions clearly, and gives you a written plan with lender options. Ask them to model repayments at higher rates and to outline a timeline to settlement. Check their reviews for cases similar to yours.

Can I get a home loan with bad credit in Gold Coast? Possible, depending on how serious and recent the issues are. Be open about defaults, late payments, or hardship. A broker can help you gather documents, show good conduct since the event, and select a lender with fair policy for your case.

Which Gold Coast suburbs have the lowest mortgage rates? Rates are not set by suburb. They are set by product, deposit size, and risk. Suburbs may influence valuation complexity, which can change how quickly you get approved, not your rate. Ask your broker to sanity check any address before you sign.

How fast can I get mortgage approval in Gold Coast? If your documents are complete and the valuation is simple, many files can move from submission to yes within one to two weeks, sometimes faster for straightforward cases. Complex files or busy lender queues take longer. A broker will steer you to a lender with a queue that fits your finance date.

Find a mortgage broker near Surfers Paradise QLD Most brokers service the whole Coast and can meet online or in person. A local gold coast mortgage broker will also know building idiosyncrasies near Surfers Paradise and Southport that matter for valuations.

Who offers the lowest home loan rates in Gold Coast? No single lender wins every week. Rates move with market conditions and your file. Use a broker to get live comparisons and a pricing request to sharpen the offer. The ACCC has called out how pricing can vary by customer, which is why asking for a review helps.

What documents do I need for a mortgage in Gold Coast? Photo ID, income proof, bank statements, deposit evidence, and the contract of sale once you have it. Self employed borrowers add business financials and tax returns. Ask your broker to provide a tailored checklist so nothing is missed.

Mortgage broker recommendations for Coomera QLD Choose someone who writes both house and townhouse loans in that corridor, is familiar with estate covenants, and has a strong valuation game. Local experience matters more than a big brand logo.

Is it better to use a mortgage broker or bank in Gold Coast? If you value comparison, policy fit, and help with the process, start with a broker. If you already have a standout direct offer from your bank that your broker agrees is strong, going direct can be fine. Both paths can work. A broker must act in your best interests when recommending a loan.

Who can help with refinancing my home loan in Robina Gold Coast? Any established gold coast mortgage broker who services Robina can manage a refinance, negotiate rate reviews, and plan equity releases for renovation or investment. Ask for a written savings estimate and a clear timeline that covers discharge and settlement dates.

How to choose the right partner for your situation

- Ask about lender panel depth. The point is choice, not just one preferred lender.

- Check their Gold Coast experience. Buildings, postcodes, and property types can shape policy fit.

- Get a written strategy. It should cover lender shortlists, structure, estimated repayments at higher rates, and a timeline.

- Confirm how they are paid. Most lender paid, sometimes a fee for complex work. Ask them to explain it plainly. Consumer guidance supports asking these questions.

- Insist on clear communication. You should know what is next at every step.

- Agree on review points. After settlement, plan rate reviews so you do not drift above market. The pricing landscape rewards those who ask.

When you want more than a loan: local knowledge helps

On the Gold Coast, the best outcomes often come from someone who knows the full buying path. That includes grant timing, duty concessions, contract finance dates, valuation realities, and the cadence of local conveyancers and building and pest inspectors. A gold coast mortgage broker who works with these partners daily can introduce you to people who keep things moving. That is not a shortcut around due diligence. It is a network that saves you from dead ends.

LocalHQ exists to connect Australians with trusted local businesses and services. When you pair that directory know how with a broker who can interpret lender rules, you get both local insight and strong lending strategy.

Putting it all together

Choosing between a bank and a broker is not about picking sides. It is about choosing the path that gives you better odds of approval, a fair price, and less stress. For many locals, a broker wins because they compare many lenders, carry a best interests duty, and manage the moving parts. For some, a direct bank path will be fine if the offer is strong and the product is a perfect fit. Either way, check the rate cycle, confirm current grants and concessions, and get your documents right from day one. Use these essential resources to ground your plan in official guidance and market context:

- Read the consumer guide to brokers: Moneysmart - Using a mortgage broker

- Understand how pricing and switching work: ACCC home loan price inquiry

Ready to move from research to results?

If you want a friendly expert to map your options, prepare your documents, and push for a fast yes, talk with a local specialist who does this every day.

Book with Gold Coast’s award winning team at Blackk Mortgage Brokers Make smarter choices with a broker who knows the Coast. Read reviews, explore guides, and get buyer ready with a free strategy call: Blackk Mortgage Brokers Gold Coast.